Home / Life Insurance / Articles / Why is Employer Life Insurance Not Enough?

Why is Employer Life Insurance Not Enough?

TeamAckoMay 20, 2026

Share Post

Employer life insurance may not be enough. It offers limited coverage and ends when you leave the job. This creates a sudden financial gap in case of a critical need. The employer-provided life insurance limitations include coverages that cannot be carried forward if you change jobs, insufficient coverage amounts, and are limited to no customisation to suit your long-term goals. So, if you are confused whether to continue with employer life insurance or buy a personal plan, keep reading.

Contents

What are the Advantages of Employer Life Insurance?

Even though the coverage in employer life insurance is limited, some benefits of employer life insurance you can enjoy include:

Cost Effectiveness

Employer life insurance is very cost-effective. In some cases, the employer pays the premiums in full. You enjoy basic financial security without paying much for premiums. This becomes very convenient for employees.

No Medical Exam Required

Most employer policies do not require medical tests. This makes enrollment simple and quick. Employees with health issues can still get coverage. There is less paperwork and fewer approval delays.

Retention of Employees

Providing life insurance is a great addition to the benefits package. Employees feel more secure and appreciated. This boosts job satisfaction. Strong benefits could also encourage employees to stay longer with the company.

What are the Disadvantages of Employer Life Insurance?

Employer life insurance includes different limitations like cancellation risk, dependency on employment status and more. Here are some of the disadvantages in detail:

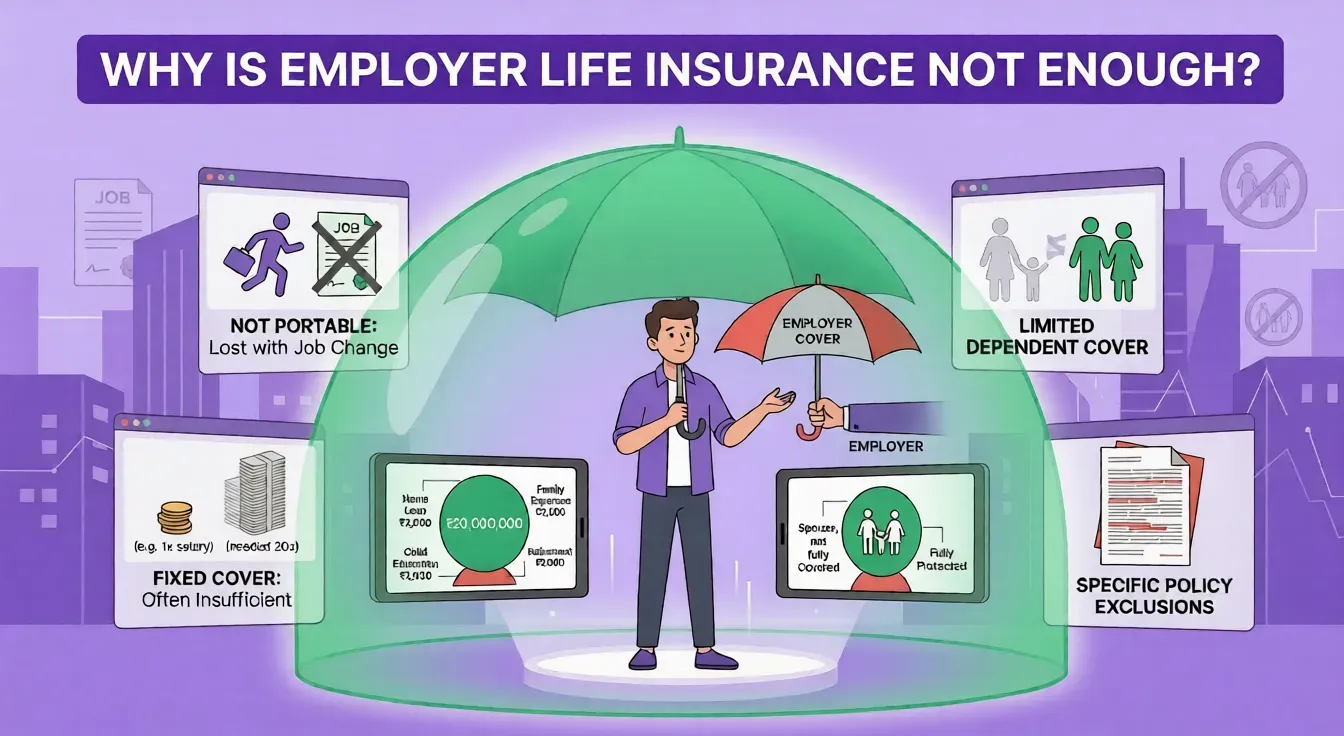

Limited Coverage Amount

The employer-provided life insurance plans provide coverage based on your salary. It is usually 1-2 times or 3 to 5 times (for senior roles) of your yearly income. For instance, if your annual income is ₹10 lakh, then your family might receive coverage of only ₹10 to ₹20 lakh.

However, replacing 10 years of income will require approximately ₹50 lakh or more. Hence, if something happens to you, then a small payout from the employer's life plan might not be enough to support the regular and long-term needs of the family.

Lack of Portability

Employer life insurance is linked to your job. This suggests that if you change or lose your job or retire, the insurance usually stops. This could leave your family without financial backup when it is still required.

Moreover, you cannot transfer the group insurance policy to a new employer. In such scenarios, buying a new plan later will cost more due to your higher age. For instance, if you switch jobs at 40, your old coverage may stop, and a new policy could be more expensive.

No Customisation or Control

The employer selects the insurer, type of policy, and the level of cover, leaving very little (if any) scope to add riders or customised cover. You cannot choose the coverage amount, duration of the policy or any additional benefits according to your individual needs.

This brings inconvenience in using your policy. For example, if you want additional critical illness cover, the employer’s life insurance plan may not offer it.

Employer Coverage is Not Permanent

Since the policy is owned by the employer, the company can change it. Employees do not have full control over their continuation. Also, if you leave your organisation, the benefit stops immediately.

Such action stops your coverage abruptly. Some companies might offer a supplemental or conversion option. Nonetheless, it generally comes at higher prices and leaves you and your family financially vulnerable in case of your sudden demise.

Cancellation Risk

Employer-provided life insurance coverage varies based on the group policy offered by the employer. Nonetheless, the life insurance coverage may be terminated if the employer chooses to discontinue, modify, or not renew the life insurance policy.

The insurers mostly provide advance notice as defined in the contract. So, in such situations, employees may lose coverage unless the employer arranges a replacement policy.

Benefits of Buying Your Own Life Insurance Plans

Personal life insurance fills the employer life insurance coverage gap by providing several benefits.

Financial Protection for Dependents

The main benefit of getting a life insurance policy is to provide financial security for your family in the event of your untimely demise. Your family may need to cover daily expenses, children's education or mortgages in your absence. If you buy an individual policy, it can cover larger sums. It is generally advised to be 15-20 times your annual salary.

Complete Control Over Coverage Decisions

You can select the policy type, coverage, policy term, premium and extra riders such as critical illness or waiver of premium all by yourself for your own life insurance policy. You can customise the plan as per your financial goals and family needs.

Policy Continues Even if You Change Jobs

Individual life insurance does not depend on your job. The policy remains active even if you switch jobs, retire or start your own business. You only need to pay the premium on time as per policy terms to continue the coverage as per your needs.

Eligibility for Tax Benefit

If you purchase individual life insurance, you can avail a tax benefit up to ₹1,50,000 on the premium amount as per section 80C of the Income Tax Act, 1988. Apart from this, the sum assured amount is tax-free under Section 10(10)D.

ACKO Life Insurance - Pure Protection, Unmixed

The life insurance product offered by ACKO is simple and easy to understand. The insurance product is designed in such a way that it provides financial security without any investment-linked benefits. The aim is to offer a simple protection solution for your family against the uncertainties of life.

ACKO Life Flexi Term Plan

The ACKO Life Flexi Term Plan provides pure term insurance coverage to policyholders. The plan pays a death claim in case the life insurance policyholder passes away during the term of the policy. However, the terms and conditions of the policy must be satisfied.

The policy allows the policyholder to choose the payment structure, either a lump sum or structured payouts. It also allows flexibility in terms of changing the sum assured and the policy term within predetermined limits. Additional riders, such as accidental death, accidental total permanent disability, and critical illness, can also be added. This helps to enhance protection as per individual needs.

What is the Difference Between Employer Life Insurance and Individual Life Insurance?

Check below to understand the difference between employer life insurance and an individual life insurance policy:

Bottom Line

Having an employer-provided life insurance is convenient, but it has several limitations. It mostly depends on your job and annual salary. It may also not provide adequate coverage to your family in case of your unexpected demise. Hence, buying your own life insurance policy offers stability as well as long-term protection to fulfil your family’s needs in your absence. It offers more control and better financial protection to your family as per policy terms.

Frequently Asked Questions

Below are some of the frequently asked questions on Why is Employer Life Insurance Not Enough?

Do all employers provide life insurance to employees?

No, not all employers offer life insurance coverage to their employees. Employer life insurance is not a legal requirement, but an optional feature of the company.

Will my employer's life insurance be valid after leaving a job?

No, usually coverage ends when you leave your job unless conversion options are offered.

Do I need to pay for employer life insurance?

Yes, employer life insurance costs are shared between the employer and the employee. You pay your portion of the amount through payroll deductions.

Is employer life insurance enough for family protection?

No, an employer group life insurance plan might not be sufficient for family protection. This is because it mostly offers limited and salary-based coverage and ends if you change jobs or retire.

How much life insurance coverage does a person need?

In general, a person must have life insurance coverage that is equal to 10 to 15 times their annual income.

Explore Life Insurance Product

Was this article helpful?

Recent

Articles

Do ADAS Features Reduce Car Insurance Premiums in India?

Nikhila PS Jun 25, 2026

How Do BS6 Bikes Affect Bike Insurance Premiums and Coverage?

Nikhila PS Jun 25, 2026

Does Health Insurance Cover Recurrent Depressive Disorder?

Neviya Laishram Jun 25, 2026

Top 15 Car Companies in India in 2026

Nikhila PS Jun 25, 2026

Does Two-Wheeler Insurance Cover Dents and Paint Damage?

Nikhila PS Jun 24, 2026

All Articles

Want to post any comments?

ACKO Term Life insurance reimagined

ARN:L0072|*T&Cs Apply

Check life insurance

#36/5, Hustlehub One East, Somasandrapalya 27th Main Rd, Sector 2, HSR Layout, Bengaluru, Karnataka 560102