Home / Health Insurance / Articles / Individual Health Insurance / Why Should Every Woman Have an Individual Health Insurance Plan?

Why Should Every Woman Have an Individual Health Insurance Plan?

Roocha KanadeDec 10, 2025

Share Post

Women play multiple roles in their family's life, taking care of them, supporting them and much more. In this daily hustle, their own health sometimes takes a backseat. Their own health is not always at priority and sometimes they might even ignore doctor visits fearing prolonged treatment and related costs.

This is why having individual health insurance for women is not just a safety net, but a strong step toward financial and medical independence. Your own policy ensures you have uninterrupted coverage, freedom to choose treatments, and long term protection as your health needs evolve. Here’s why having an individual health insurance plan is essential for every woman, at every stage of life.

Contents

- Importance of Individual Health Insurance for Women

- Financial Benefits of Having an Individual Health Insurance Plan for Women

- Health and Lifestyle Advantages for Women

- Why Women Should Not Depend Only on Family or Group Health Insurance?

- Tips for Women Buying Individual Health Insurance

- Conclusion

- FAQs on Individual Health Insurance for Women

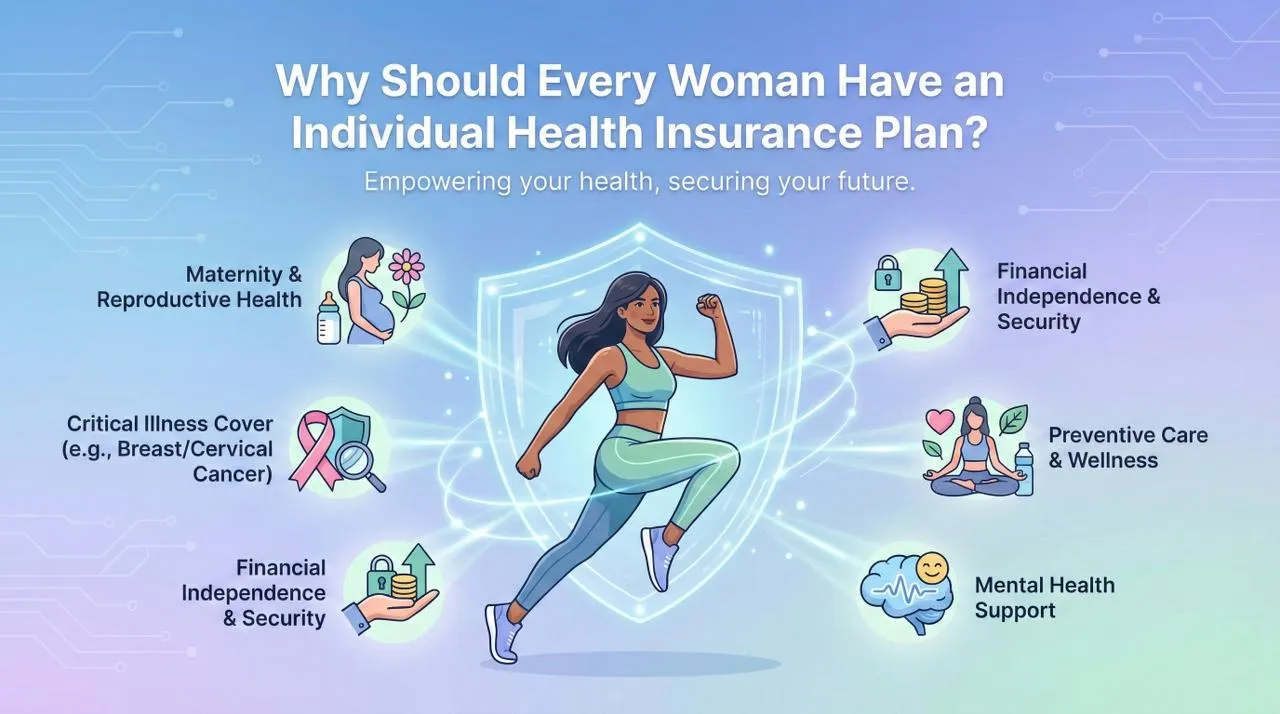

Importance of Individual Health Insurance for Women

Women face very specific health issues like thyroid disorders, reproductive health issues, breast and cervical cancer, etc. These issues need frequent treatment and regular monitoring. Additionally, maternity-related treatments and care also increase the financial burden. Moreover, healthcare costs and medical inflation is rising every year.

Having individual health insurance for women ensures medical independence. You don’t have to depend only on your husband’s plan or your employer’s group cover. Having personal coverage ensures medical independence and long-term security.

Women’s Health Statistics 2023-25

Here are some important health-related statistics for women. These profoundly increase the need for timely treatment and having a reliable health insurance plan.

Anaemia affects 57% of Indian women aged 15–49, per NFHS-5 (up from ~53% since the last survey)

In aspirational districts, the anaemia rate among women went up even more, from 58.7% (NFHS-4) to 61.1% (NFHS-5).

According to ICMR/NCRP data, breast and cervical cancers remain the top two cancers among Indian women.

In 2023, an estimated 35,691 women died of cervical cancer in India.

The 5-year survival rate for breast cancer in India is only 66.4%, per an ICMR study.

Financial Benefits of Having an Individual Health Insurance Plan for Women

Following are the financial benefits of having an Individual Health Insurance Plan for Women.

Protection Against Rising Costs: Medical inflation is rising at nearly 14% per year, so something as common as a C-section or a routine breast screening can cost far more than you expect. A reliable women’s health insurance plan helps take care of the costs and keeps your savings intact.

Continuity Beyond Employer or Spouse Coverage: Relying on an employer's health plan or being an insured member in a spouse's policy may increase dependence and could lead to delayed treatments. Instead with a dedicated policy, women can get the necessary medical help whenever required.

Tax Benefits Under Section 80D: Women can claim tax deductions for premiums paid for themselves, their spouse, and parents under Section 80D. These savings not only reduce taxable income but also encourage long-term investment in health.

Health and Lifestyle Advantages for Women

Here are some health and lifestyle advantages for women while buying health insurance.

1. Coverage for Women-specific Conditions

An individual health insurance plan for women often covers conditions like breast cancer, cervical cancer, endometriosis, infertility-related treatments, and other chronic lifestyle diseases. Having a personal policy ensures you aren’t limited to family coverage that may not fully meet these needs.

2. Access to Preventive Health Check-ups

Most plans include annual preventive check-ups. These tests help women detect hormonal issues, vitamin deficiencies, reproductive concerns, and chronic illnesses at an early stage. Early detection means easier treatment and lower costs.

3. Maternity and Newborn Coverage Options

Women planning a family can opt for maternity add-ons, which cover pregnancy costs, childbirth, and newborn care. Since maternity benefits come with waiting periods, buying your own health insurance early ensures you are covered when the time comes.

Why Women Should Not Depend Only on Family or Group Health Insurance?

Relying only on a spouse’s family plan or your employer’s group cover may leave gaps in coverage. Group plans end the moment you switch jobs. Family floater plans share one sum insured among all members. Having your own health insurance policy will ensure continuous coverage even after job change, marriage or relocation.

For example, if your husband or child gets hospitalised and uses most of the sum insured, you may have very little left for your own medical needs. This can lead to underinsurance, especially during expensive treatments or emergencies.

Getting a separate health plan for women ensures that they are not dependent for coverage on some else's plan. This provides financial back-up in case of need and peace of mind.

Tips for Women Buying Individual Health Insurance

Here are some useful tips for women who are looking to buy an Individual Health Insurance Policy.

Consider buying a health plan early as it will help you stay covered for a long time, even if you develop any health conditions later in life.

Find a health plan that offers basic coverages like maternity benefits and women-specific health issues.

Consider insurance companies with a wide network of hospitals. This will help you get the right treatment at the earliest.

If major illnesses are not directly covered under the plan then you can go for add-ons like critical illness cover or accidental disability cover.

Consider setting your sum insured to ₹5 to ₹10 lakh depending upon your location. The cost of healthcare in urban areas is more as compared to rural regions.

Use free online tools to compare health insurance plans from different companies.

Avoid relying only on employer insurance, as it ends the day you leave the job. Plan early so your health insurance grows with you, not after a medical event.

Conclusion

Health insurance is not a luxury. It is a necessity for every woman who wants financial independence and long term protection. Buying an individual health insurance plan ensures you stay covered through every stage of life without depending on anyone else.

Protect your health and secure your future, invest in an individual health insurance plan today.

Also read: Benefits of Individual Health Insurance: Why It’s Worth It

FAQs on Individual Health Insurance for Women

Below are some of the frequently asked questions on Why Should Every Woman Have an Individual Health Insurance Plan?

Why should women have a separate health insurance plan?

Women should have a separate health insurance plan to get financial protection in case of situations like job change, marriage, etc.

Does individual health insurance cover pregnancy?

Yes, many plans offer maternity and newborn add-ons, but they come with waiting periods.

Can I buy health insurance for my mother or daughter?

Yes, you can purchase separate individual plans for them based on their age and health needs.

What is the ideal coverage amount for women?

A sum insured of at least ₹5 to ₹10 lakh is recommended, especially for those living in metro cities.

Explore More Articles on Individual Health Insurance

Explore Our Comprehensive Health Insurance Options

Recent

Articles

Family Health Insurance vs Individual Health Insurance: Key Differences

Roocha Kanade Dec 10, 2025

Why Should Every Woman Have an Individual Health Insurance Plan?

Roocha Kanade Dec 10, 2025

Advantages of Individual Health Insurance for People Aged 20 to 35

Roocha Kanade Dec 10, 2025

Top Reasons Why Individual Health Insurance Applications Get Rejected

Roocha Kanade Dec 10, 2025

How Pre-existing Diseases Impact Your Individual Health Insurance Premiums

Roocha Kanade Dec 10, 2025

All Articles

Want to post any comments?

Discover our diverse range of Health Insurance Plans tailored to meet your specific requirements🏥

✅ 100% Room Rent Covered* ✅ Zero deductions at claims ✅ 7100+ Cashless Hospitals

Check health insurance

Acko Technology & Services Private Limited

#36/5, Hustlehub One East, Somasandrapalya, 27th Main Rd, Sector 2, HSR Layout, Bengaluru, Karnataka 560102

Acko Group Companies:

Download our ACKO app now!

Products

Company

Support

Car Insurance

Bike Insurance

Health Insurance

- Health Insurance

- Health Insurance Plans

- 10 Lakhs Health Insurance

- 50 Lakhs Health Insurance

- 1 Crore Health Insurance

- Health Insurance Plans For Family

- Individual Health Insurance

- Cashless Health Insurance

- Women's Health Insurance

- Health Insurance For Parents

- Health Insurance For Senior Citizens

- Health Insurance Premium Calculator

- Waiting period in health insurance

- Health Insurance Portability

- Super Top Up Health Insurance

Group Health Insurance

Travel Insurance

CIN: U74110KA2016PTC120161

The use of images and brands are only for the purpose of indication and illustration.