Home / Life Insurance / Articles / How to Get Term Insurance with Pre-Existing Conditions

How to Get Term Insurance with Pre-Existing Conditions

Neviya LaishramFeb 17, 2026

Share Post

Having a pre-existing medical condition does not automatically disqualify you from getting term insurance. Contrary to popular belief, it is possible to buy term life insurance with pre existing medical conditions. While it is true that the process of buying insurance might take longer for those with pre-existing conditions, term insurance can nevertheless be bought by any individual to secure the future of their loved ones.

This article covers the basics of buying term insurance with pre existing medical conditions, what are the rules governing it and what you can expect when looking to buy affordable life insurance.

Contents

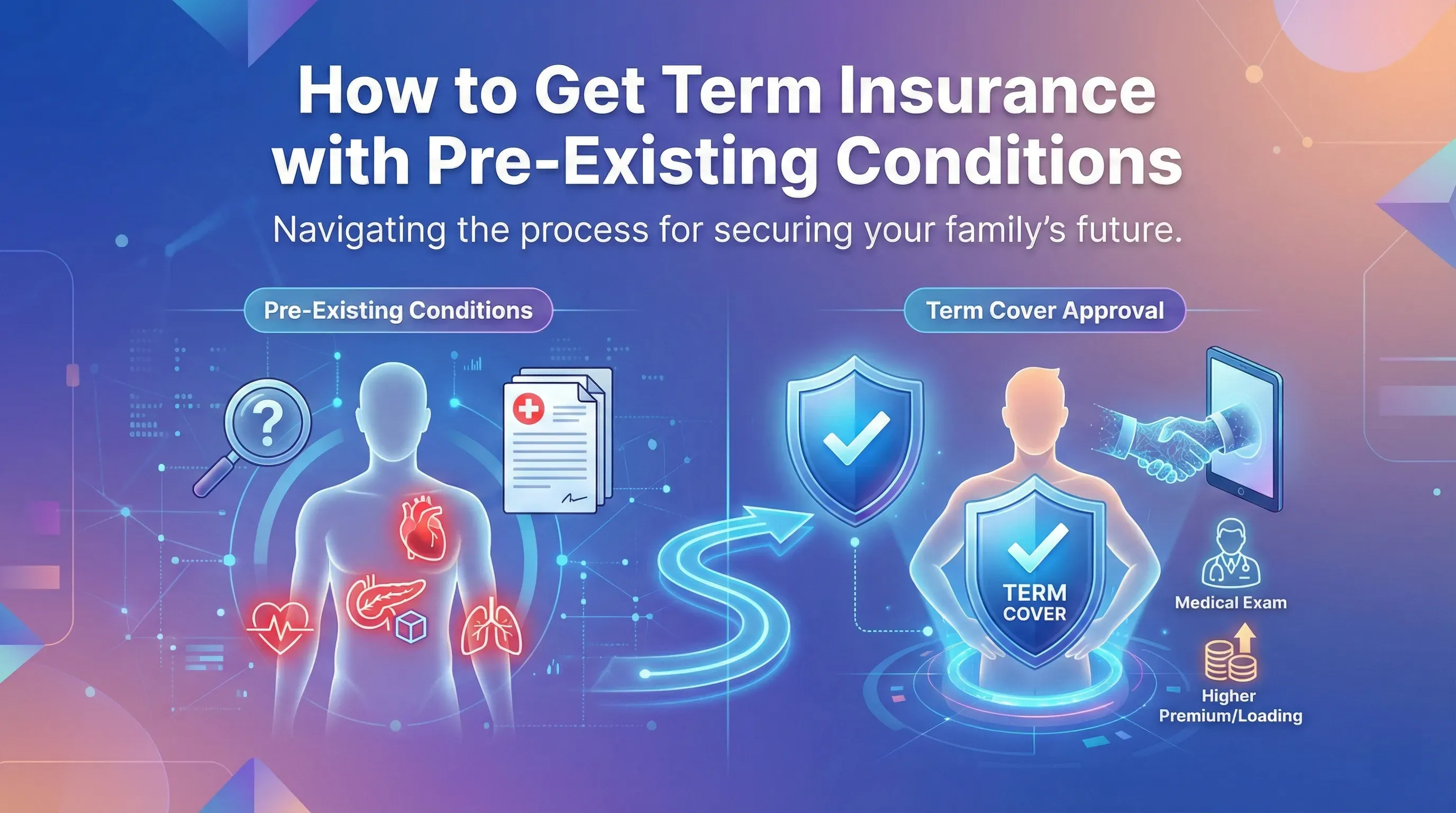

What are Pre-Existing Conditions

Chronic illnesses, including diabetes, hypertension, asthma, thyroid disorders, and severe diseases such as heart disease and cancer, are some examples of pre-existing conditions. Insurance Regulatory and Development Authority (IRDAI) defines them as conditions diagnosed, showing symptoms, or treated within 48 months before policy purchase.

Due to the increased risk of mortality associated with these conditions, insurers require extensive underwriting processes. It involves review of previous medical records and documentation, current laboratory reports (e.g., HbA1c for diabetics, lipid profiles for hypertensive patients), and the patient's current and historical lifestyle behaviours. It is done to assess if the patient will be subject to a loading on their premium, be excluded from certain policy benefits, or may be denied coverage based on the severity of the condition.

Understand What Counts as a Pre-Existing Condition

Any illness or health issue diagnosed before buying the policy is considered pre-existing. Common examples include:

Diabetes

High blood pressure

Asthma

Thyroid disorders

Heart conditions

Even past conditions that are under control must be disclosed.

IRDAI Rules for Life Insurance Pre-Existing Condition

The IRDAI requires all insurers to evaluate applications for life insurance pre-existing conditions.

Underwriting-based Decisions: The decision of an insurer to approve is based on the medical report, the age of the applicant, their lifestyle, and their overall risk profile while evaluating insurance for pre-existing medical conditions. The insurer will apply the appropriate wait period, exclusions, or premium loading.

Premiums are loaded for Manageable Conditions: This allows applicants to obtain affordable life insurance while acknowledging they have a health risk.

Transparency and Protection for the Policyholder: IRDAI's recent updates emphasise clear communication terms, exclusions, and loading by insurers. This prevents policyholders from being denied claims unfairly in relation to life insurance pre-existing condition disclosures.

How to buy term insurance for pre-existing medical conditions?

Follow these steps for better chances of approval:

Be truthful: Provide all your medical records, prescription drugs, visits to doctors, and lab test results that meet the insurer’s testing criteria. By doing this, you can get your insurance company's trust to prevent them from denying your claim in the future.

Get Multiple Term-Life Insurance Quotes Online: Use calculators to compare premiums based on age, sum assured, lifestyle, and pre-existing medical conditions.

Determine How Much Coverage You Need: Assess income, liabilities, dependents, and future goals to select adequate life cover before proceeding.

Medical Screening: You may be required to undergo medical tests, such as blood sugar, ECG, or lipid profiles. Some plans offer term life insurance no medical exam, subject to underwriting criteria.

Compare the Various Term-Life Insurance Plans: Look for flexible options, such as pure or level term life insurance, and check how much premium loading is applied if you have a pre-existing condition. Also, review the availability of optional riders, such as critical illness cover.

Read Your Policy: Read the policy document carefully to understand premium loadings, exclusions related to pre-existing conditions, and all applicable terms and conditions before making the payment.

Buy Term-Life Insurance Digitally: Choose an online platform to avoid paying agents' commissions, save money, and get approved faster.

With the right approach, you will have the ability to secure the financial well-being of your family members regardless of their current or previous medical status.

Digital insurance platforms such as Acko Life Insurance make it easy to purchase term life insurance. Learn about the ACKO Life Flexi Term Plan.

Factors That Influence Approval and Premium Loading

Insurers may load premiums but extend cover after review

Conclusion

Securing term insurance with pre-existing medical conditions may seem difficult at the outset. However, if you disclose all information, compare plans thoroughly, and are aware of what IRDAI has in place regarding these types of applications, securing a term life policy will be possible.

Frequently asked questions

Below are some of the frequently asked questions on How to Get Term Insurance with Pre-Existing Conditions

What are pre-existing conditions in life insurance?

Pre-existing conditions in life insurance are any illnesses, diseases, or health issues that were diagnosed, showed symptoms, or required treatment before you bought the policy.

Can I buy term insurance if I have a medical condition?

Yes, you can buy term insurance even if you have a medical condition. Most insurers offer coverage after assessing the severity and control of the condition. You may be approved at a higher premium, with certain exclusions, or after medical tests.

Will my premium be higher if I have a pre-existing condition?

Yes. Insurers may charge a higher premium (premium loading) depending on the severity, stability, and management of your condition.

Can my term insurance claim be rejected due to a pre-existing condition?

A claim is usually rejected only if the condition was not disclosed at the time of purchase. If you declare your medical history honestly and the policy is issued, then claims will be paid as per the policy terms.

Explore Life Insurance Product

Was this article helpful?

Recent

Articles

Do ADAS Features Reduce Car Insurance Premiums in India?

Nikhila PS Jun 25, 2026

How Do BS6 Bikes Affect Bike Insurance Premiums and Coverage?

Nikhila PS Jun 25, 2026

Does Health Insurance Cover Recurrent Depressive Disorder?

Neviya Laishram Jun 25, 2026

Top 15 Car Companies in India in 2026

Nikhila PS Jun 25, 2026

Does Two-Wheeler Insurance Cover Dents and Paint Damage?

Nikhila PS Jun 24, 2026

All Articles

Want to post any comments?

ACKO Term Life insurance reimagined

ARN:L0072|*T&Cs Apply

Check life insurance

#36/5, Hustlehub One East, Somasandrapalya 27th Main Rd, Sector 2, HSR Layout, Bengaluru, Karnataka 560102